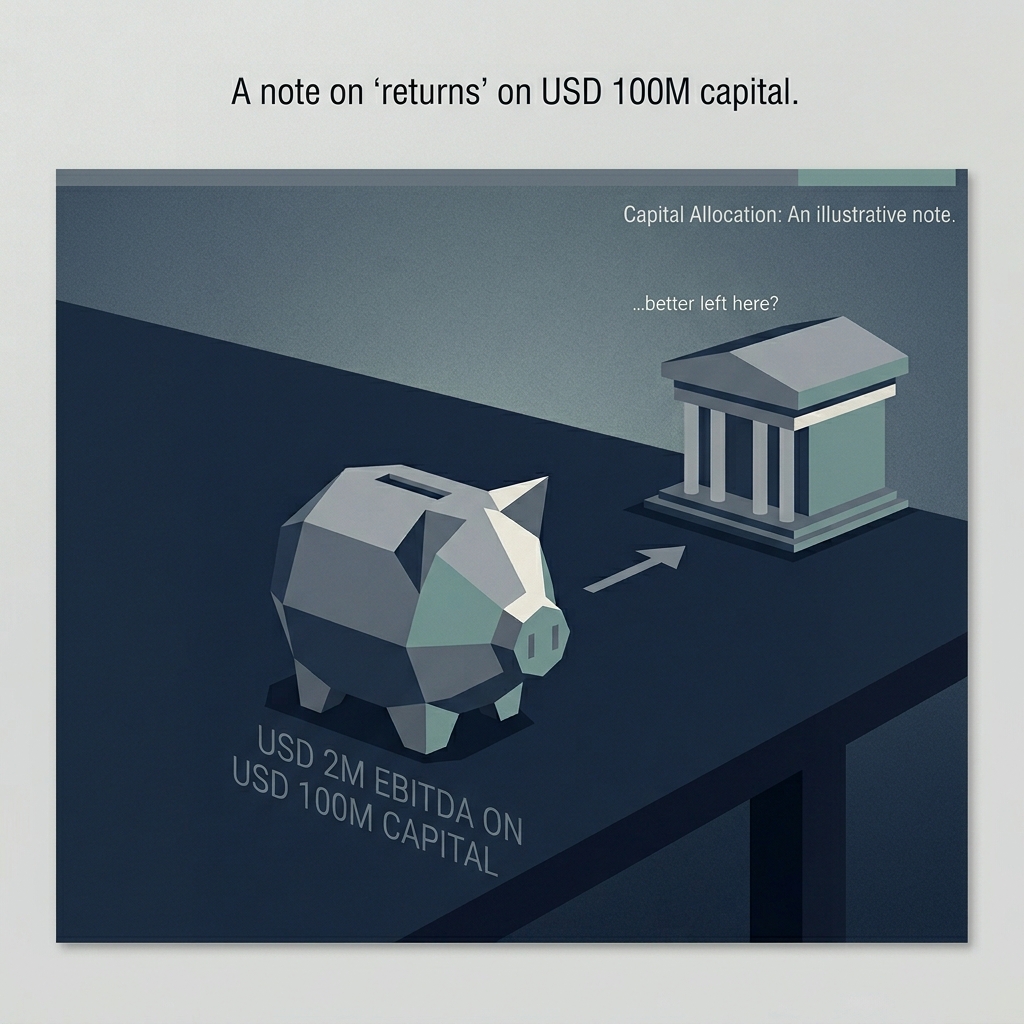

Imagine a distributor who generates USD 2 million in EBITDA on a capital base of USD 100 million. They pay their staff, cover their overhead, and show an operating profit at the end of the year. By conventional viability standards they are fine - positive EBITDA, cash in the bank, a real business.

They are also economically irrational. A 2% return on capital employed is worse than what the same distributor could earn by liquidating the business, depositing the capital in a local bank, and going on a long holiday. In countries where informal lending rates run 10–15%, a 2% ROIC isn't a bad business - it's an absurd one. Yet I've seen distributor viability frameworks approve exactly this profile because the EBITDA test passed.

The error is foundational. It comes from treating EBITDA and ROIC as substitutable measures of the same thing - profitability - when in fact they measure two different and independent conditions. EBITDA answers: is the operation covering its operating costs? ROIC answers: is the capital deployment justified relative to the opportunity cost of that capital? A business must pass both tests to be viable. Passing one is necessary but not sufficient.

Here is how the failure mode typically unfolds. A tenant designs a distributor P&L model. The model includes cost of capital as a P&L line item - the distributor's working capital is X, the financing cost is X × annual borrowing rate ÷ 12, and this becomes a monthly cost reducing EBITDA. The model then also runs an ROIC test: EBITDA ÷ capital employed, compared to a hurdle rate (borrowing rate + 30% risk premium, or whatever the tenant has decided is appropriate).

That model double-counts. The financing cost goes into the cost base, which reduces EBITDA. Then the ROIC test applies the hurdle rate to the already-reduced EBITDA, which effectively penalizes the distributor for the cost of capital twice. You get artificially low viability numbers and approve distributors who shouldn't have been approved, because the model has made the test harder than it was meant to be on paper and then adjusted the threshold down to compensate.

The correct architecture separates the tests cleanly.

EBITDA is pure operating profit. Cost of capital comes out of the P&L entirely. EBITDA = revenue − (direct costs + overhead costs) with no financing line. This is what the business actually earns from operations before any consideration of how it's financed.

ROIC is the capital return test. ROIC = EBITDA × 12 ÷ capital employed. The hurdle rate is the cost of capital plus a risk premium. The test is binary: does ROIC exceed the hurdle? Pass or fail.

Viability requires both conditions independently. EBITDA must be positive - otherwise the business isn't covering its costs. ROIC must exceed the hurdle rate - otherwise the capital should be deployed elsewhere. Both tests must pass. Passing one and failing the other is not a viable distributor.

This has a counterintuitive implication that took me some time to accept: the distributor's leverage choice is irrelevant to the viability test. Whether they fund the business with 100% equity or 80% debt shouldn't change whether the business is viable. The business either earns above the hurdle on capital deployed, or it doesn't. Leverage is a financing decision made after the viability question is answered. Building leverage into the viability model conflates the two.

In practice this means you run the ROIC test leverage-agnostic. Calculate capital employed as if the distributor funded 100% of it themselves. Apply the hurdle rate. If ROIC clears the hurdle, the business is viable regardless of how it's actually financed. If it doesn't, leverage won't save it - leverage will amplify the loss.

This reframing has three practical consequences for any commercial organization that works through distributors.

First, it changes what a viable distributor looks like. A distributor generating USD 5M EBITDA on USD 50M capital employed (10% ROIC) in a country with a 15% borrowing rate and a 30% risk premium target (hurdle rate ~19.5%) is not viable, no matter how healthy the EBITDA number sounds. The capital they've tied up is earning below the opportunity cost. The tenant needs to either help them reduce capital employed, increase margin, or accept that the relationship will erode as the distributor reallocates attention to businesses that pay better.

Second, it changes the business case for the tenant. If a tenant is asking a distributor to invest capital - inventory, receivables, warehouse, vehicles - the tenant is implicitly asking the distributor to earn above the hurdle rate on that investment. If the math doesn't work, the tenant is asking the distributor to subsidize them. That is not a sustainable relationship regardless of how warm the personal chemistry feels.

Third, it creates a pair of levers for fixing an unviable distributor. Unviable ROIC can be fixed in three ways: reduce capital employed (smaller territory, less inventory, faster collection), increase margin (better mix, higher ASP, reduced cost-to-serve), or accept a lower ROIC target for strategic reasons (the tenant invests in the distributor's shortfall, explicitly and visibly, for a defined period). Naming the lever is what moves the conversation from "this distributor isn't performing" to "here is what specifically needs to change."

There's one more point worth making, which is about the conversation with the distributor's owner.

Owner-operators of distributor businesses rarely think in ROIC terms. They think in cash flow, employment for their people, and relationships. When you walk them through the ROIC framework - this is what your capital is earning, this is what it could earn if you put it somewhere else, this is the gap - something shifts. Either they commit to closing the gap or they realize they should be doing something else. Both outcomes are better than the alternative, which is quietly extending a relationship that both parties know isn't working and neither party has the framework to discuss.

The EBITDA-only viability test is how distributor relationships die slowly and unexplained. The EBITDA-and-ROIC viability test is how they get fixed, or ended cleanly, with both parties able to see what happened.

If you work through distributors and your current model only tests one condition, add the second. It will reclassify 10–30% of your distributor base. Some will become viable that didn't look it. Some will become unviable that did. In both cases you will be closer to the truth of what the business is actually worth.

Let me walk through a specific worked example, because the arithmetic makes the principle concrete in a way that the abstract framework doesn't.

Consider a distributor in Jakarta handling automotive lubricants. Their monthly revenue is USD 800k at a 16% distributor margin, giving gross profit of USD 128k. Their monthly operating costs - DSR team, warehouse, logistics, overhead - total USD 95k. Their monthly EBITDA is USD 33k, or USD 396k annualized. That's a real business.

Their working capital requirement is USD 2.1 million (inventory float plus trade receivables net of tenant credit). Their fixed asset base - warehouse, vehicles, equipment - is USD 900k. Total capital employed is USD 3 million.

ROIC = USD 396k / USD 3 million = 13.2%.

Indonesia's informal borrowing rate is around 14%. Apply a 30% risk premium and the hurdle rate is 18.2%.

The distributor's ROIC of 13.2% is below the hurdle of 18.2%. By the ROIC test, the business is unviable. Capital employed here would earn better returns if redeployed elsewhere.

But notice: the EBITDA test passes. The business covers its operating costs with USD 33k to spare each month. A framework that only applies the EBITDA test classifies this distributor as viable and moves on. A framework that applies both tests identifies the ROIC gap and names it specifically: capital employed is too high for the margin structure. The distributor needs to either reduce capital employed (tighter working capital management, perhaps by renegotiating tenant credit terms or adjusting receivables policy) or increase margin (product mix shift toward higher-margin SKUs, better pricing discipline).

Both paths are actionable. Neither is visible if the framework doesn't apply the ROIC test.

The framework also applies to the distributor-to-tenant conversation, and this is where I've seen it change outcomes.

When the distributor's owner sees the ROIC calculation - their own capital earning 13.2% against an 18.2% hurdle - the conversation shifts. They don't dispute the math; the math is straightforward. What they often say is: "I never thought about it that way. I knew the business was tight, but I assumed it was because of operational issues. I didn't realize the capital I have tied up here is earning less than it would in the bank."

This realization is usually followed by one of three outcomes. Some distributors commit to closing the gap - they work with the tenant on a specific plan to reduce capital employed or increase margin, with milestones and a defined timeline. Some distributors decide to exit - they conclude that the capital should be redeployed to their other businesses, and they either sell the operation or wind it down over an agreed period. A few distributors become combative - they argue the hurdle rate is too high, the risk premium too generous, the framework unfair.

All three outcomes are better than the alternative, which is the distributor continuing to operate a capital-losing business because no one showed them the arithmetic.

One nuance worth noting: the ROIC hurdle rate should itself be configurable, not hardcoded. Different markets have different risk profiles, different opportunity costs, and different capital mobility characteristics. A 30% risk premium over the informal borrowing rate is a reasonable default for emerging Asian markets. It's too low for markets with volatile currencies or thin banking systems, and too high for mature markets with developed alternatives. The tenant should set the risk premium at onboarding, based on market context and their own investment thresholds.

Similarly, the capital employed calculation should explicitly separate working capital from fixed assets, because the levers are different. Working capital can be adjusted within months through receivables policy, inventory management, and credit terms. Fixed assets are multi-year decisions. A distributor whose ROIC gap is driven by high working capital has a different action plan than one whose ROIC gap is driven by oversized warehouse and vehicle investment.

The granularity matters because the conversation with the distributor has to specify which lever to pull. "Your ROIC is below hurdle" is a statement. "Your ROIC is below hurdle because your working capital requirement has grown 40% over eighteen months while your margin structure stayed flat" is a diagnosis. The diagnosis points to the intervention. The statement points nowhere.