The lubricants category in Indonesia has a statistic that stops most territory-modelling frameworks in their tracks: 14% of category volume now transacts through e-commerce platforms. Tokopedia, Shopee, Lazada, Blibli - mostly value-seeking consumers buying direct, bypassing the traditional workshop-and-petrol-station channel structure that every distributor territory is designed around.

14% isn't a rounding error. A distributor P&L that assumes full access to the category's addressable volume is overstating viability by exactly that amount. If the model predicts a territory can support a distributor earning IDR 200 million a month in EBITDA, and 14% of the territory's consumers are actually buying from e-commerce platforms that the distributor doesn't touch, the real number is IDR 172 million - a 14% hit to the viability case. Some territories that look marginal under the standard model would be clearly unviable under the realistic one. Conversely, the model's own confidence in any territory's P&L is artificially inflated by a structural assumption that hasn't been checked.

This is the kind of problem that tempts a lazy fix. "Add a note to the deck about e-commerce exposure." The note is read as a caveat, the model numbers are accepted as-is, and the structural issue goes unaddressed. A year later, a distributor is underperforming against plan and nobody can explain why. The explanation was in the footnote that nobody operationalised.

The right fix is to make e-commerce cannibalisation a first-class variable in the model.

The variable

We introduced `ecommerce_cannibalization_rate` - a tenant-configurable, territory-overridable percentage that represents the share of a category's addressable volume flowing through e-commerce in a given market. Indonesia: 14%. Malaysia: 8%. Thailand: 11%. These numbers come from a mix of third-party market reports, the client's own sell-in data (which shows the gap between addressable market and physical-channel throughput), and senior partner override where the data is thin.

The variable feeds a new derived quantity: `R1-adj = R1 × (1 - cannibalization_rate)`. R1 is the total addressable market volume; R1-adj is the portion of that volume that can realistically flow through the physical distributor channel. Every distributor P&L in a "Managed Parallel" posture - meaning the brand operates both physical and e-commerce channels alongside each other - calculates on R1-adj, not R1. The distributor's revenue, margin, and viability verdict are all computed against the realistic addressable volume.

The cannibalisation rate carries a confidence tier like every other variable. In Indonesia for the lubricants category, we have enough third-party data to rate it MEDIUM confidence. For a category where no market data is available, it would start as LOW confidence and be flagged for upgrade through field research or client-provided sell-through comparison.

Three strategic postures, not just one rate

The variable isn't only a number. It sits inside a strategic posture decision that the senior partner makes for each engagement. Three postures are possible, each with its own treatment of the e-commerce channel:

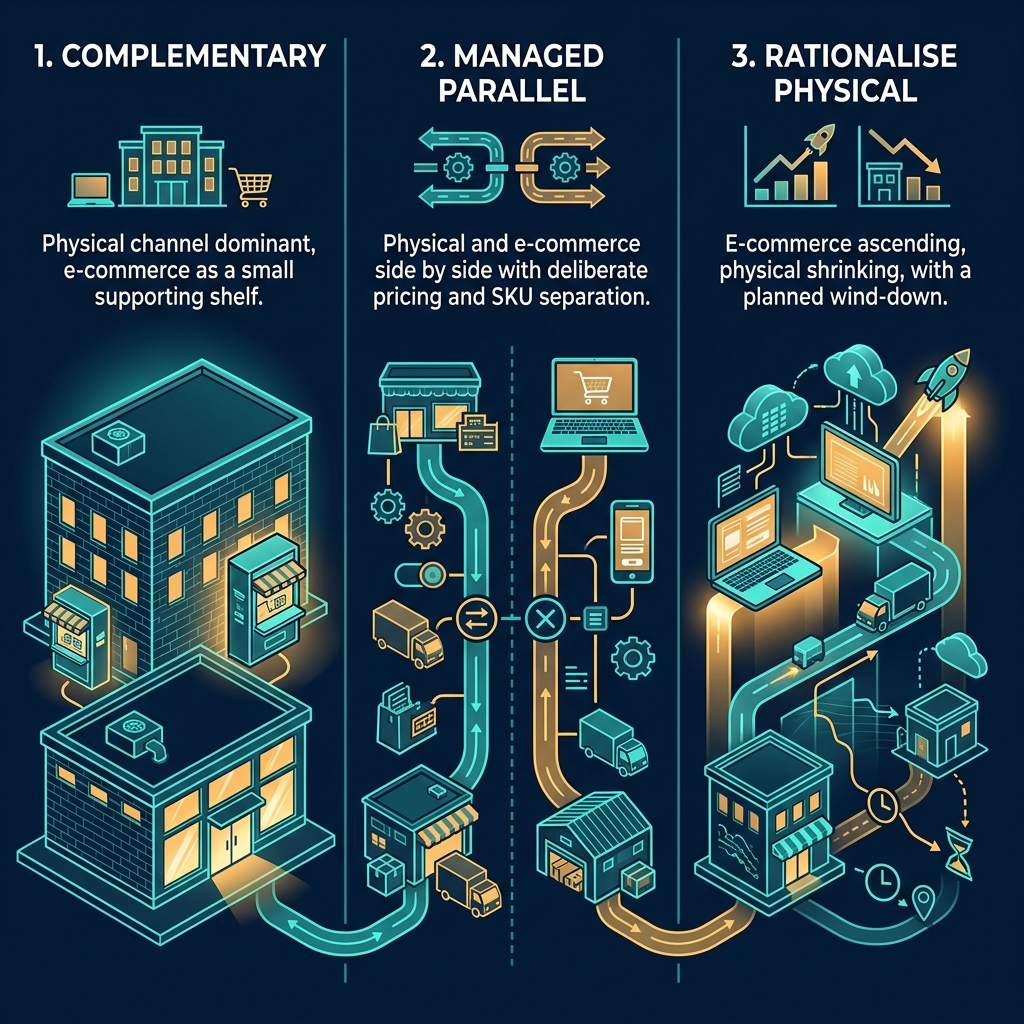

"Complementary" - the brand treats e-commerce as a minor channel for the category. Cannibalisation is low, perhaps under 3%. The physical channel is the dominant access point, and the e-commerce presence is mostly about brand visibility. R1-adj roughly equals R1. This posture fits mature categories where the physical channel has defensive strength.

"Managed Parallel" - the brand operates e-commerce alongside physical with deliberate coexistence. Cannibalisation is material but bounded (8-15%). R1-adj is meaningfully less than R1. The brand invests in both channels, manages pricing to prevent channel conflict, and ring-fences certain SKUs or territories for each channel. Most categories in Southeast Asia are here. This is where the adjustment to the distributor P&L is most important.

"Rationalise Physical" - the brand accepts that e-commerce is structurally taking share from physical. Cannibalisation is high (20%+) and rising. R1-adj is materially less than R1. The conversation with physical distributors is honest: "your territory is shrinking 8% a year because of e-commerce. We will invest in retaining you, but we're not pretending the physical channel will grow." This posture fits categories in transition - parts of personal care, some consumer electronics, increasingly parts of FMCG.

The posture choice is a strategic conversation the SP has with the client, not a default. It sits on a dedicated slide in the engagement deliverable, with a confidence-rated cannibalisation estimate and a clear implication for each territory's P&L.

Why this needs to be a deck-level conversation

E-commerce cannibalisation being a footnote in the territory analysis is a failure of commercial honesty. It tells the physical distributor that their territory supports a certain economic model, while privately knowing that the model overstates by 14%. The distributor, six months later, finds their volume underperforming plan, doesn't know why, and loses trust in the platform.

Treating cannibalisation as a first-class variable forces the honest conversation up front. The distributor is told: "your territory's R1-adj is 172 million litres, not 200 million. The gap reflects e-commerce exposure that this brand manages separately. Your P&L, your DSR plan, your working capital model all run on R1-adj." The conversation is different in kind. The distributor is partnered in the reality, not deceived by the projection.

It also changes the brand's relationship with the distributor. A distributor told their territory is shrinking 8% a year because of e-commerce can plan for it - can adjust their fleet size, their DSR count, their credit terms, their exit strategy. A distributor who only sees the R1 number and hears vague disclaimers feels betrayed when reality lands. The structural honesty is a form of respect.

The broader principle

Any structural force that materially affects an addressable market needs first-class treatment in the model, not footnote treatment. E-commerce is the obvious example for retail categories, but the pattern applies elsewhere. Direct-to-consumer shifts in categories where brands are building owned channels. Subscription models in categories moving from transaction to recurring revenue. Regulatory changes that redefine product categories or access rights. Platform aggregators that take share from traditional distribution.

The diagnostic for whether something deserves a first-class variable is simple: if it changes an addressable market number by more than a single-digit percentage, it's first-class. A 14% cannibalisation rate that's hidden as a footnote destroys the model's usefulness. The same 14%, surfaced as a first-class variable with its own confidence tier, posture-dependent treatment, and explicit deck-level conversation, makes the model more trustworthy, not less.

Good commercial models don't hide uncomfortable variables. They make them checkpoints. Every uncomfortable variable that gets first-class treatment is one fewer place where reality will ambush you later. The discipline of surfacing them upstream is the discipline that separates a model you can bet on from a model that looks sophisticated and fails in operation.