Every regional distribution strategy eventually encounters the territory that doesn't work. The market isn't big enough to support a dedicated distributor at viable scale. The geography is too dispersed for efficient coverage. The incumbent competition is too strong for a challenger to establish a standalone operation. Whatever the specific cause, the conclusion is the same: this territory cannot carry a dedicated distributor's fixed cost base.

The conventional options at this point are two. Activate anyway and subsidize the distributor until the territory grows into viability - expensive, slow, often fails. Or don't activate and accept the coverage gap - costs the tenant revenue and leaves the territory to competitors. Most organizations choose some combination, with the usual result that marginal territories are chronically underserved and periodically reviewed without conclusion.

There is a third option that most organizations either don't consider or misconceive when they do. It is the shared infrastructure model, and it works - but only if you get the economics right.

Here is the concept. In a marginal territory there is often an existing distributor who services a different, non-competing category. Let's say the tenant is a confectionery brand entering a rural province in Indonesia. A local distributor in that province already handles cookies and snacks from other principals. That distributor has warehousing, delivery vehicles, and a DSR team whose routes cover the territory's priority outlets. Adding the tenant's confectionery products to that distributor's book is operationally trivial - same outlets, same routes, same relationships, a different product on the same truck.

The question is how to structure the economics.

The wrong way to structure this - and the way most organizations attempt it - is as a service arrangement. The tenant pays the shared distributor a service fee (per case handled, per visit, or a monthly retainer). The tenant retains margin, the distributor earns a logistics fee. This is how most people describe the shared infrastructure model when they first encounter it.

It doesn't work. Service fee arrangements are only used in practice by pure-play logistics providers - third-party distribution companies whose entire business is paid handling. When you try to impose a service fee on a multi-category distributor who also handles their own principals, several things go wrong. The distributor has to track costs at a level of granularity they don't normally maintain. Their incentive is volume of handling, not volume of the tenant's product sold. Their relationship with the tenant becomes transactional rather than commercial. And most importantly, the arithmetic often doesn't work - the service fee needed to make the distributor whole is higher than the tenant can afford while still pricing competitively in the territory.

The right way to structure the economics is as a partnership, not a service.

The shared distributor takes on the tenant's product line as a secondary principal. They earn the tenant's distributor margin - whatever the tenant pays its dedicated distributors in other territories. They sell the product through their existing channels, alongside their primary-category products. The tenant doesn't pay a service fee. The distributor doesn't charge one.

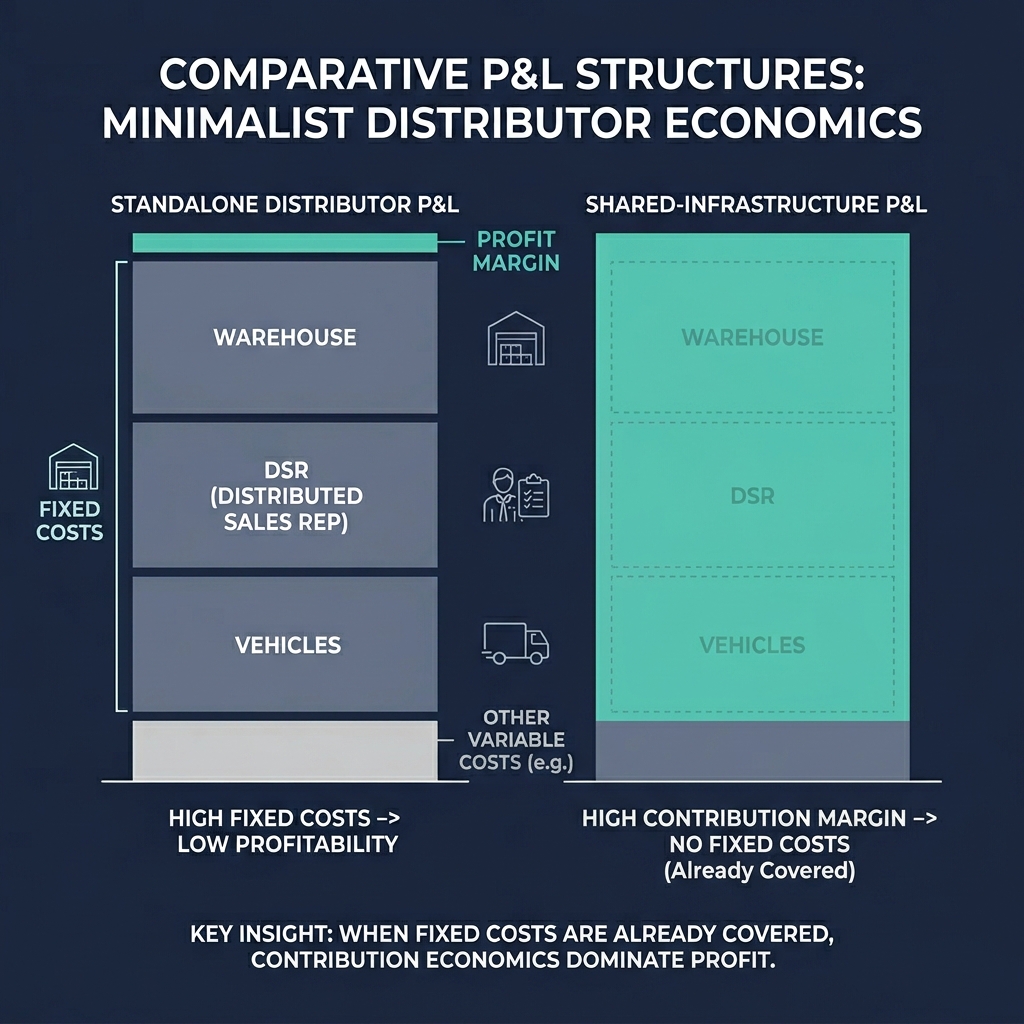

Here's why this works. The distributor's fixed costs - warehouse rent, DSR salaries, vehicle operations, route planning - are already covered by their primary-category business. Adding the tenant's products doesn't meaningfully increase those costs. The DSRs visit the same outlets. The trucks run the same routes. The warehouse has spare capacity by definition (if it didn't, the distributor couldn't have taken the tenant on). The marginal cost of adding the tenant's product to the business is, for most practical purposes, close to zero.

Revenue, on the other hand, is real. Every unit of the tenant's product the distributor moves generates incremental gross margin. That margin flows almost entirely to profit, because the costs that would normally offset it are already covered. The distributor's P&L for the tenant's product line shows strong contribution margins from the first unit sold.

The distributor's investment in the tenant's product is working capital - inventory float and trade receivables for the tenant's products specifically. That's the economic commitment. And the distributor's risk is default risk on trade credit extended to outlets for the tenant's products. That's the commercial exposure. Both are manageable at the scale of a secondary category.

The viability test for the shared infrastructure model is dramatically simpler than the standalone test. There is no fixed cost threshold to cross. The test is: does the incremental gross margin exceed the working capital cost plus the bad debt provision? If yes, the distributor earns profit from the first unit. If no, the model doesn't work. Pass/fail, unit one.

This changes what "viable" means in marginal territories. A territory that cannot support a dedicated distributor at any volume may well support a shared distributor at low volume - because the fixed cost bar that made the territory unviable standalone simply isn't there. The territory becomes contribution-positive even at modest penetration.

Three specific conditions determine whether the shared infrastructure model will work in a given territory.

First, there needs to be an adjacent non-competing distributor whose existing routes physically pass through the tenant's target outlet clusters. This is a geospatial compatibility check, not a category overlap check. Outlet types can be different - a cookie distributor and a confectionery distributor may list in different outlet types - but if the routes go to the same geographic clusters, the shared economics work. Outlet-type matching is not what matters. Route compactness is.

Second, the tenant's product must generate meaningful contribution margin within the shared distributor's cost envelope. If the tenant's margin is thin enough that the working capital cost eats most of it, the model doesn't work even structurally. The contribution has to exceed the financing cost plus bad debt with real margin to spare - otherwise the distributor's reward for the partnership is too small to motivate prioritization.

Third, the territory must not be so attractive that diluted distributor commitment is the binding constraint. This is the one condition that limits the model's applicability. In a high-attractiveness territory, the tenant wants a distributor whose whole attention is on the tenant's business. A shared distributor by definition splits attention between principals. That's acceptable when the territory's upside is modest. It's expensive when the upside is large. So the shared infrastructure model is explicitly for low-to-medium attractiveness territories, never for high-attractiveness ones.

There is one design principle worth emphasizing because organizations get it wrong. In the shared infrastructure model, owner compensation is genuinely zero - not declared zero as a reporting convention, but actually zero as economic reality. The distributor owner's time is already absorbed by the primary-category business. Adding the tenant's product does not require any incremental owner attention at the management level. So the owner salary line in the shared model's P&L is truly zero. This is the only context in which a zero owner salary is an honest number rather than a distortion. Don't impute one. Don't adjust for it. It's really zero.

The shared infrastructure model should be recommended, when it applies, as a first-class option alongside dedicated distribution and do-not-activate. In my experience, organizations that build the option into their territory design explicitly - with the compatibility check, the margin test, and the attractiveness constraint all formalized - recover somewhere between 15% and 30% of the territories that would otherwise be classified as unreachable. That's a significant portion of the market, and it's available at low risk precisely because the economic model is cleaner than the standalone alternative.

The shared infrastructure model isn't new, exactly. Distributors have been handling multiple principals forever, and savvy brand managers have been using informal versions of this arrangement for decades. What's new is formalizing it as a deliberate strategic option, modeling its economics correctly, and embedding it in the territory design process rather than leaving it as an opportunistic workaround.

When a territory comes back marginal, the question shouldn't be "do we activate or don't we." It should be: "can we find the right shared distributor here?" That's a different question with a different answer, and the answer is available more often than most organizations realize.

The practical mechanics of identifying a shared infrastructure candidate are worth walking through, because this is the part most organizations underestimate.

The shared distributor is rarely found through the tenant's existing distributor sourcing processes, because those processes are built around finding dedicated distributors. The candidates for shared infrastructure come from different channels entirely. The tenant's broader distributor network - relationships in other markets and categories - is one source; a distributor handling FMCG snacks in one province may have an adjacent cousin operation handling the same category in the target province. Field research during Module 1 identifies another category of candidates - non-competing distributors mentioned in trade interviews, seen in outlet observations, or identified through public business registers. Senior Partner networks - the consulting relationships that the strategy partner brings into the engagement - surface a third channel of candidates.

The identification process benefits from being explicitly non-AI. AI can help filter candidates against structural criteria (route compactness, outlet overlap, category compatibility), but the qualitative assessment of whether a distributor is a credible partner for the tenant is a commercial relationship judgment. Does the distributor's owner have capacity for a secondary principal? Do they have the operational discipline to handle a new product line without degrading their primary business? Are they the kind of partner the tenant wants to be associated with in the territory? These are questions that require human judgment, and the Senior Partner's role in the engagement is precisely to make that judgment.

Three failure modes are worth naming, because organizations that attempt the shared infrastructure model without awareness of them tend to discover them the hard way.

Failure mode one: the shared distributor underinvests. Because the fixed costs are already covered by their primary category, the marginal effort required to support the tenant's product is low. This sounds like a feature and it often is. But it also means that when the territory needs more attention than the shared distributor is giving it, there's no financial lever to force the investment. The distributor is already earning contribution margin on whatever volume they move - they have no inherent pressure to scale. If the tenant wants the territory to grow beyond the distributor's ambient effort level, the tenant has to create that pressure directly, usually through growth-linked incentive structures that sit above the standard distributor margin.

Failure mode two: channel conflict with the primary category. Even when the categories are technically non-competing, the shared distributor's outlets notice that the same DSR is now pushing a second product line. The outlet's relationship with the DSR becomes more complex. Purchase decisions on the primary category can get entangled with purchase decisions on the tenant's category, sometimes in ways that hurt both. This is particularly acute when the tenant's product has different margin economics from the primary category - if the tenant's product offers better margin to the outlet, the outlet may substitute it for primary-category purchases, cannibalizing the distributor's main business. The distributor then sees the tenant's product as a threat to their primary P&L and starts deprioritizing it, regardless of the incremental contribution. The compatibility check has to consider this dynamic, not just route compactness.

Failure mode three: governance gaps. In a dedicated distributor relationship, the tenant has clear lines of authority over the distributor's commercial execution for the tenant's product. In a shared infrastructure relationship, the shared distributor's commercial authority remains with their primary business, and the tenant is operating as a secondary principal with less direct influence over execution decisions. When something goes wrong - a stock-out, a pricing dispute, a trade program that underperforms - the tenant's options for intervention are more limited than in a dedicated relationship. The shared distributor's responsiveness is a function of their own priorities, and the tenant is not always at the top of the list.

Each of these failure modes has mitigations. Growth-linked incentives address the underinvestment problem. Explicit category boundaries in the commercial agreement address channel conflict. Senior relationship management and clear governance protocols address the responsiveness gap. None of the mitigations eliminate the underlying tension; they manage it. An organization using the shared infrastructure model at scale needs to build these mitigations into the standard contract structure and the standard operational cadence.

There is also a cultural dimension to how the shared infrastructure model is communicated within the tenant's organization.

Dedicated distributor relationships are the norm in most commercial organizations. The sales director, the regional commercial manager, the business development lead - all of them grew up in an environment where "a distributor" meant "a dedicated partner who carries our product exclusively or near-exclusively in their territory." Shared infrastructure feels different to these people. It feels like a compromise. It feels like admitting the territory wasn't worth a real distributor. Some of that instinct has to be actively managed.

The shared infrastructure model is not a compromise - it's a different shape of commercial relationship, suited to a different set of territory economics. When it's framed as "the solution for markets that couldn't justify a real distributor," it carries stigma that undermines the relationship from the start. When it's framed as "the right structure for mild-to-moderate attractiveness territories where fixed-cost leverage of an adjacent operator is economically superior to a dedicated operation," it carries the dignity it deserves.

The framing matters because the shared distributor will pick it up. If the tenant's team treats the relationship as second-class, the distributor will treat the tenant's product as second-class. If the tenant's team treats it as a strategic choice for a specific market context, the distributor will match that energy. The model works best when both parties agree on what it is and why it's the right structure for this territory.

A final thought on when not to use the shared infrastructure model.

The model is inappropriate in high-attractiveness territories for reasons already discussed - diluted commitment is too expensive when the territory's upside is large. It's also inappropriate in markets where the tenant is aggressively trying to establish a premium brand position, because the shared distributor's identification with multiple categories can muddy the brand positioning in ways that the tenant can't fully control. It's inappropriate in markets with sensitive regulatory requirements (pharma, food safety) where the handling of the tenant's product needs to be dedicated and traceable.

Outside those constraints, the model is broadly applicable and underused. For organizations willing to commit to the required discipline - correct economic modeling, careful candidate identification, explicit governance protocols, and an honest framing of the relationship - it opens territories that would otherwise remain unreachable. That's a significant portion of the market in most categories.