When we first designed the SKU channel fit score, the brief was practical: which SKUs should a distributor push through which channels? The question is concrete, the audience (commercial director, distributor principal) is clear, and the data needed (SKU attributes, channel characteristics, margin economics) is available. It felt like a straightforward weighted-average problem. Four components, weights, a 0-to-100 score per SKU-channel pair.

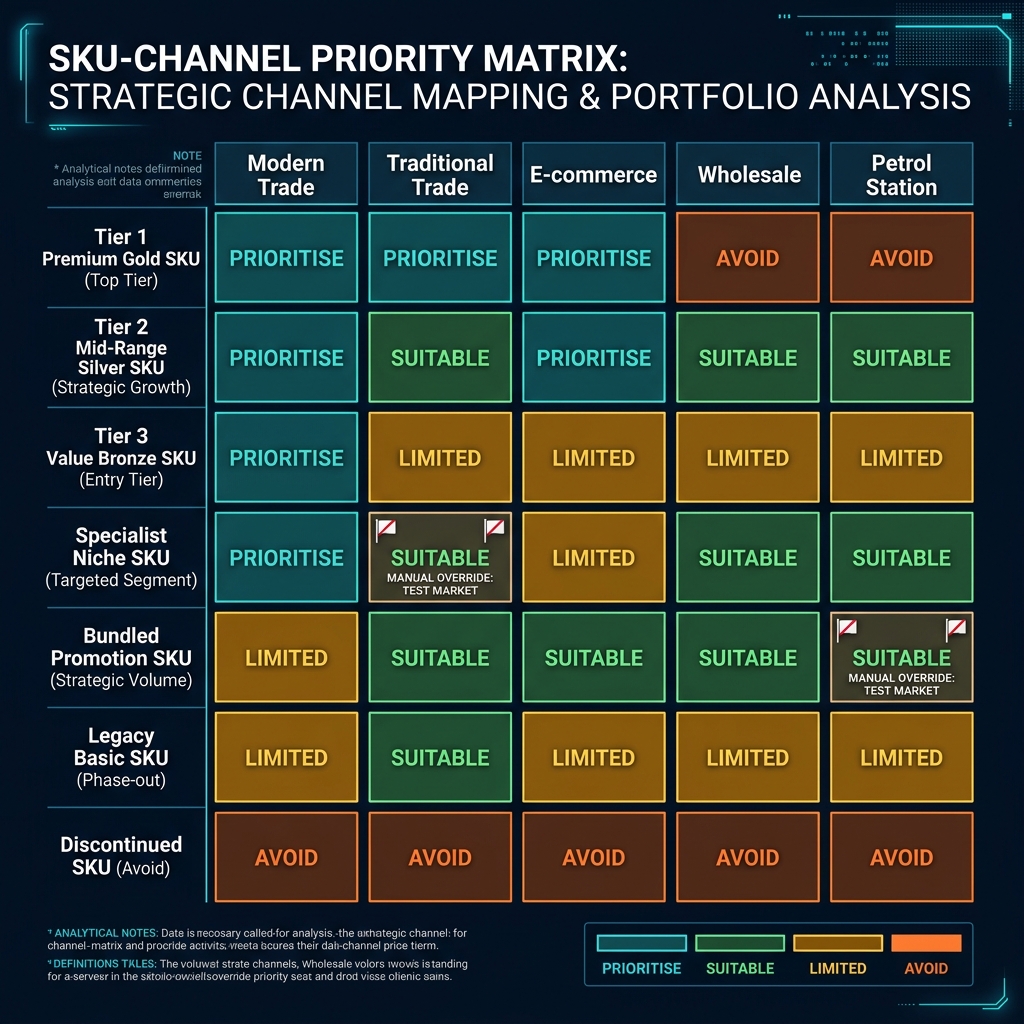

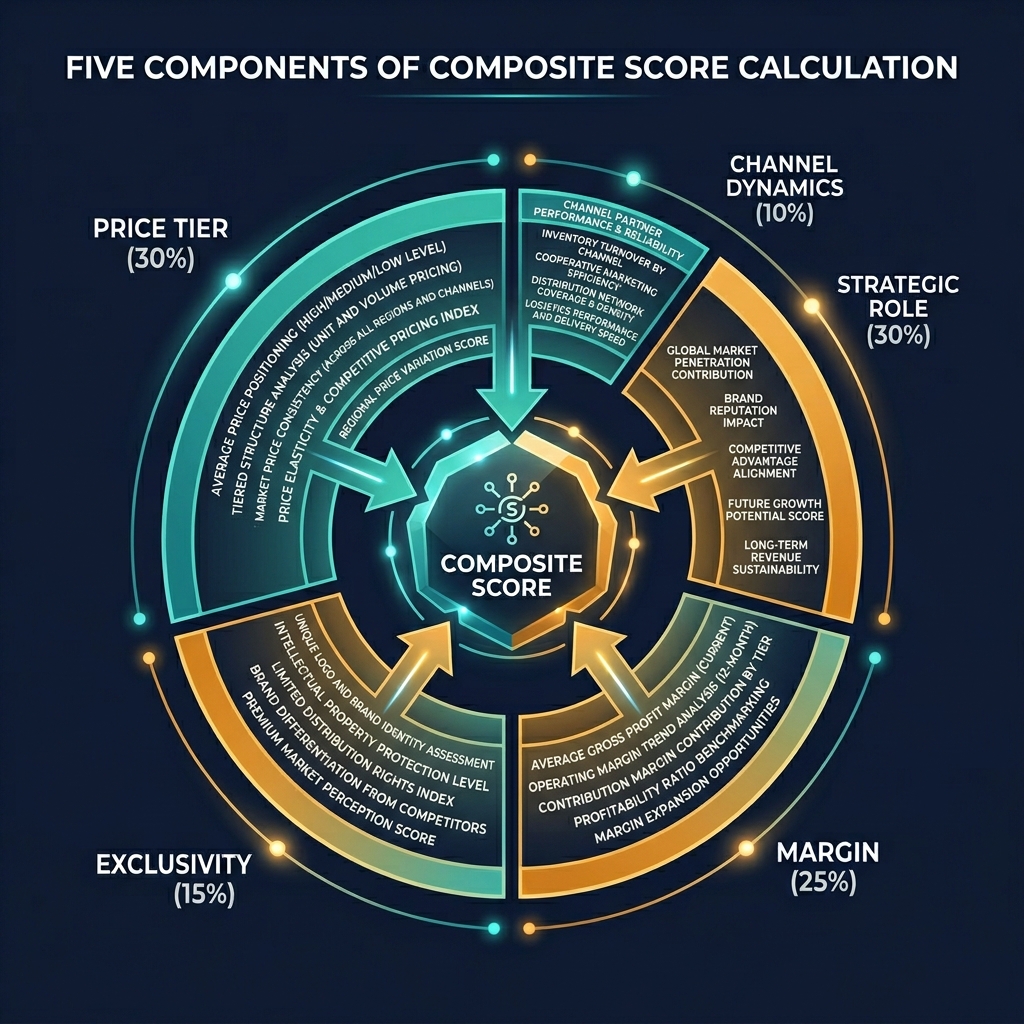

The formula that emerged looks respectable on paper. Price Tier fit (30% weight) - how well does the SKU's price positioning match the channel's typical consumer? Strategic Role fit (30%) - is this a hero product going to mass channels or a margin product going to premium channels? Margin Sustainability (25%) - does the channel's cost structure support the SKU's margin economics? Channel Exclusivity (15%) - does the distributor have exclusive rights in this channel, justifying investment? Compute each component on a 0-to-100 scale, weight them together, and you get a score. Above 90, PRIORITISE. 65-89, SUITABLE. 40-64, LIMITED. Below 40, AVOID.

The model works. It's defensible. It gives the SP and distributor a starting point for channel-by-channel investment conversations. Good enough for the first pass, we thought.

Then the reality check. We started running the model against actual SKU portfolios in actual Southeast Asian markets, and the scores came out subtly wrong.

The first anomaly: premium in e-commerce

The model gave premium SKUs a score of 90 for e-commerce channels - high priority, treat it as a major investment target. This is the correct answer in most Western markets, where e-commerce consumers are brand-aware, higher-income, and willing to pay premiums for authenticated, premium-positioned products.

It is the wrong answer in Southeast Asia. Shopee, Tokopedia, Lazada - the dominant platforms - are built around value-seeking consumers looking for deals. Premium positioning in these platforms is actively undermined by the platforms themselves: "lowest price" sorting, aggressive discount promotions, one-click comparison, seller reviews that punish any perceived premium pricing as "expensive" or "overpriced". A premium SKU dropped onto Shopee without careful price management gets compared unfavourably to a cheaper competitor within thirty seconds of a consumer's search.

The score should reflect this. Premium × e-commerce in Southeast Asia is not PRIORITISE (90). It's LIMITED (55). Investment in this combination is likely to underperform because the platform economics work against premium positioning.

The fix is to adjust the Price Tier fit component to reflect market-specific channel dynamics. Premium × e-commerce scores differently in markets where e-commerce skews value-seeking (SEA) versus markets where it skews brand-aware (much of Europe and North America). The weight stays the same; the matrix values differ by market.

The second anomaly: trade-driven versus consumer-driven

The bigger reveal came when we looked at the model's treatment of distinctly different category types. A lubricants SKU and a snack SKU, both positioned as "mid-tier hero" products, were getting similar scores for similar channels. But the underlying commercial dynamic is completely different.

Lubricants are trade-driven. The purchase decision is heavily influenced by a trusted intermediary - the mechanic, the workshop owner, the petrol station attendant. Consumers rarely select a lubricant by brand unprompted; they buy what the mechanic recommends. Marketing spend concentrates on the trade; consumer-facing marketing is less important.

Snacks are consumer-driven. The purchase decision is made by the consumer at the shelf, often impulsively. Brand recognition, packaging, shelf position, and price are the drivers. The trade plays a role (listing decisions, shelf space) but the ultimate persuasion is direct-to-consumer.

A weighted-average channel fit score that treats these the same is missing the point. A trade-driven SKU in a modern trade channel (where the shelf is impersonal and the consumer picks without guidance) is structurally disadvantaged. A consumer-driven SKU in a traditional trade channel (where the shopkeeper's recommendation matters) is similarly disadvantaged. These aren't edge cases; they're the dominant dynamic in their respective categories.

We added a fifth component to the score: Channel Dynamics fit (10% weight). A lookup matrix of TRADE_DRIVEN × channel and CONSUMER_DRIVEN × channel values. Traditional trade scores 100 for trade-driven SKUs, 70 for consumer-driven. Modern trade scores 60 for trade-driven, 100 for consumer-driven. The component adjusts the overall score in ways the weighted average couldn't reach.

From tactical score to portfolio question

With both corrections in place, the score finally matches commercial intuition. But the more interesting shift happened in how the SP uses it. The original framing was "which SKUs should we push through which channels?" - a tactical question, one SKU-channel pair at a time. The corrected framing is "how does our portfolio map to our channel structure?" - a strategic question that looks at the whole grid.

Open the SKU-by-channel matrix for a territory. See which cells are PRIORITISE (teal), SUITABLE (green), LIMITED (amber), AVOID (orange). Now ask: is our portfolio well-matched to our channel investment? A lubricants portfolio heavy on premium SKUs, with a distributor whose channel mix is 40% wholesale and 30% petrol station, is fundamentally misaligned. The premium SKUs don't fit wholesale (price sensitivity) or petrol stations (convenience-driven). Most of the distributor's effort is going to channels that don't match the brand's portfolio strategy. The fix isn't tactical - push the premium SKU harder in wholesale - it's strategic: either the portfolio needs more mid-tier SKUs to match the distributor's channel strength, or the distributor needs to shift their channel mix.

The matrix becomes a portfolio diagnostic, not an investment allocator. It's asking "are you selling the right products through the right channels?" at a portfolio level, and the answer often indicates structural decisions - product launches, channel exits, distributor restructures - not tactical tweaks.

The override protocol

Any AVOID verdict (below 40) requires SP override with written justification. The reasoning: the model can be wrong, and there are edge cases where an AVOID combination is strategically correct for non-commercial reasons - brand presence, competitive blocking, contractual obligation. The override is allowed, but it's captured in the audit log with the SP's reasoning, so the decision is visible and defensible in subsequent reviews.

The override protocol turns a computational score into a commercial gate. The model doesn't dictate; it surfaces. The SP's judgement is required for any exception. Every exception is documented. The audit trail becomes a record of commercial reasoning over time - useful in itself when the engagement is reviewed months or years later.

What this pattern teaches

The SKU channel fit score started as a tactical formula and became a strategic tool. The path was: build the formula simply, test against reality, adjust components when reality contradicts, add components when commercial dynamics demand, and eventually notice that the matrix view of all SKU-channel pairs tells a portfolio story the individual scores don't.

The general principle: tactical tools often evolve into strategic ones when exposed to enough reality. The evolution isn't a redesign; it's an accumulation of corrections that, at some point, changes how people use the tool. You can't design for the strategic use up front, because you don't yet know which corrections will accumulate. You have to build the tactical tool, run it against reality, and let the strategic framing emerge. The discipline is to stay open to the emergence rather than insisting the original tactical framing is complete.

Vertical platforms that stop at the tactical framing miss the larger payoff. A channel fit score that's only used one SKU-channel pair at a time is worth something. The same score viewed as a portfolio matrix, with accumulated market-specific corrections and strategic overrides, is worth an order of magnitude more. Most of that extra value comes from features you didn't design - filter controls, matrix visualisations, override audits - built to support use patterns that emerged after the core formula was in place.